Solution Found!

Suppose that the risk-free zero curve is flat at 6% per annum with continuous

Chapter 25, Problem 25.24(choose chapter or problem)

Suppose that the risk-free zero curve is flat at 6% per annum with continuous compounding and that defaults can occur at times 0.25 years, 0.75 years, 1.25 years, and 1.75 years in a 2-year plain vanilla credit default swap with semiannual payments. Suppose that the recovery rate is 20% and the unconditional probabilities of default (as seen at time zero) are 1% at times 0.25 years and 0.75 years, and 1.5% at times 1.25 years and 1.75 years. What is the credit default swap spread? What would the credit default spread be if the instrument were a binary credit default swap?

Questions & Answers

QUESTION:

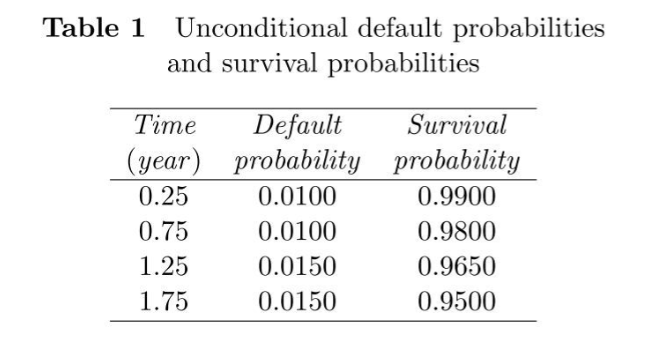

Suppose that the risk-free zero curve is flat at 6% per annum with continuous compounding and that defaults can occur at times 0.25 years, 0.75 years, 1.25 years, and 1.75 years in a 2-year plain vanilla credit default swap with semiannual payments. Suppose that the recovery rate is 20% and the unconditional probabilities of default (as seen at time zero) are 1% at times 0.25 years and 0.75 years, and 1.5% at times 1.25 years and 1.75 years. What is the credit default swap spread? What would the credit default spread be if the instrument were a binary credit default swap?

ANSWER:Step 1 of 3

The analysis is below as,

Therefore, the PV of expected payments is 3.6082s, the PV of the expected payoff is 0.0375, and the PV of the expected accrual payment is 0.0234s.

3.6082s+0.0234s=0.0375 and s = 0.0103, i.e., the credit default swap spread is 103 basis points.